How to Navigate the Maze of Social Security Survivors Benefits

In my many years of working with my clients, there is nothing more heartbreaking than seeing them lose loved ones — especially a spouse.

All circumstances are different, but the one similarity is how confused and overwhelmed they seem when managing their finances in the future. This is especially true when the spouse who passed away handled the finances daily.

The Social Security Administration steps in and tries to help with this confusion and grief by providing income to the families of spouses eligible for Social Security benefits. These are called survivors benefits or widow or widower benefits.

A widow (female) or widower (male) can start receiving reduced benefits as early as age 60 or full benefits at full retirement age for those who lost their spouse. Benefits can start as early as age 50 if you are disabled.

Who is Eligible to Receive Benefits?1

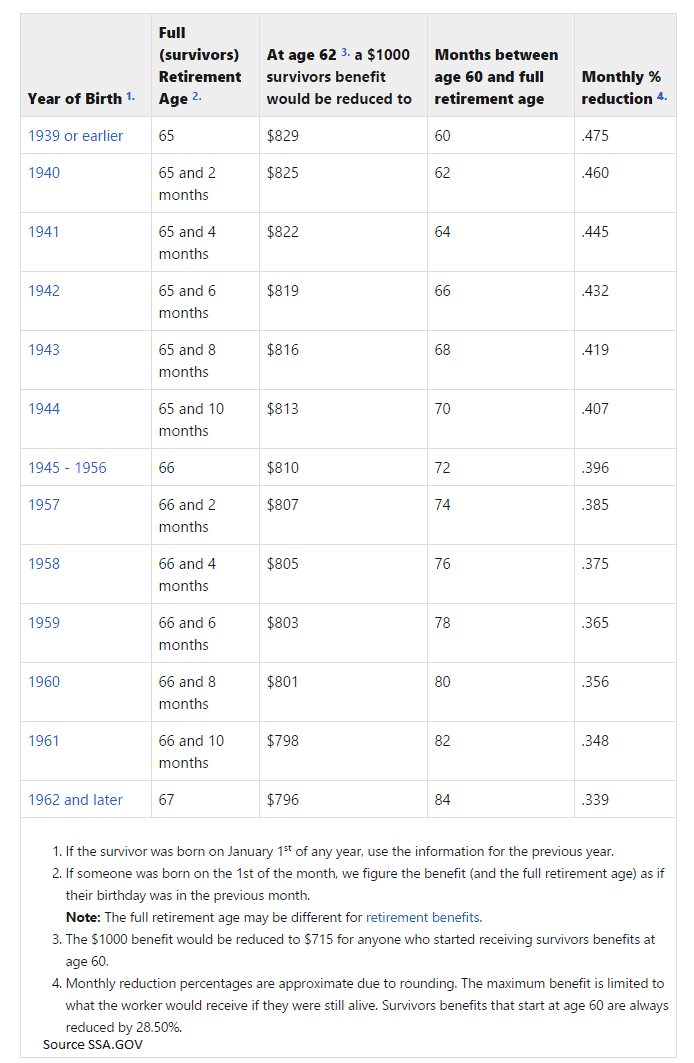

Your widow or widower may be able to get full benefits at full retirement age for survivors. The full retirement age (FRA) for survivors is age 66 for people born in any year from 1945 through 1956. The age gradually increases to age 67 for people born in 1962 or later.

A widow or widower can start receiving reduced benefits as early as age 60 or full benefits at full retirement age for survivors. Benefits can begin as early as age 50 if you are disabled.

Your widow or widower may be eligible for benefits at any age if they take care of your child younger than age 16 or if they are disabled and the child is receiving Social Security benefits.

Your unmarried children may be eligible for benefits if they are younger than age 18 or up to age 19 if they attend high school full-time. Your children can get benefits at any age if they were disabled before age 22 and remain disabled.

Interesting fact: 98 out of every 100 children are eligible for benefits if a working parent dies. I was shocked at how large this number is. Social Security pays more benefits to children than any other federal program.

Your dependent parents can get benefits if they’re age 62 or older. For your parents to qualify as dependents, you would have to provide at least half of their support.

Retirement Portion of Survivors Benefits

I’ll focus on the retirement portion of survivors’ benefits for the remainder of the article.

Many of you are probably unaware that there are two sets of full retirement ages. Many financial planners are not aware — I did not know until I was researching this topic some time ago. The full retirement age for survivors benefits can be up to four months earlier than for retirement and spousal benefits that I outline in my other article.

Dual Entitlement

The spouse is entitled to the larger benefits based on their earnings record or survivors benefits based on the husband or wife’s record.

For example, we have a husband and a wife both born the same year, the husband filed for his benefit at his full retirement age of 66, and his primary insurance amount is $2,000 per month. His wife has a primary insurance amount of $1,500 and filed for her benefits at her full retirement age of 66.

The husband passes away at age 68, and the wife now has the option to choose between her benefit and her husband’s survivor’s benefit of his primary insurance of $2,000.

Please note, however; she does not get both benefits — she would receive the higher benefit only.

Look at the same scenario, and let’s assume the husband still passes away at age 68, but in this example, he did not start taking his benefits at full retirement age 66. Instead, he was delaying his benefits and taking advantage of his delayed retirement credits of approximately 8% per year to age 70.

The wife would receive his delayed retirement credit amount of $2,320 per month rather than his primary insurance amount of $2,000 per month if he started taking benefits at his full retirement age of 66. Please read my other article, The Basics: Full Retirement Age and Social Security, for more information on delaying credits.

The wife’s survivors’ benefits reflect any delayed retirement credits at the time of the husband’s death. However, it is important to realize that they do not continue to accrue — she will get the benefit he was receiving or was eligible to receive based on his date of death.

The wife has a choice to make. She could choose to delay her retirement benefits and accumulate credits to age 70. If her full retirement age is 66 and she delays her benefits until age 70, her credits would be approximately 32% higher; benefits accrue at about 8% per year until age 70.

What this looks like in practicality is the wife starts receiving her survivor’s benefit based on the husband’s benefits. Then she would be able to switch to her retirement credits if they are higher than her survivor’s benefits at age 70, for example. Please refer to the first case study below for more on this strategy.

Am I able to claim my survivors benefit early, or do I have to wait for my full retirement age for survivors?

The surviving spouse can start benefits as early as age 60, and you can switch to your own retirement benefits as early as age 62. Why would you do that? Great question. I promise we will address this in our case studies.

The catch is if you start benefits as early as age 60, you will only receive 71.5% of the survivor’s primary insurance amount benefits. If you wait until full retirement age, you will receive the full benefit for survivors based on their primary insurance amount. If your spouse’s primary insurance at their death was $1,000 per month, you would only be entitled to $715 per month.

For example, if you’re a survivor born in any year from 1945 through 1956, your full retirement age for survivors is 66. Here are examples of what your benefit would be reduced to per SSA.gov:

- If you start receiving benefits at age 60, you will get 71.5% of the monthly benefit.

- If you start receiving benefits at age 62, you will get 81% of the monthly benefit.

- If you start receiving benefits at age 65, you will get 95.3% of the monthly benefit.

What if my deceased spouse claimed their benefit early before their full retirement age?

This is when things really start to get fun — I mean complicated. Don’t worry, that is why you made the wisest decision of your life and found my blog (joking). ☺

Suppose your spouse started taking their benefits before their full retirement age. In that case, there’s an important distinction we need to make: are you filing for your spousal benefit before your full retirement age for survivors or when you reach your full retirement age?

Suppose you are filing at or after your full retirement age. In that case, it is much less complex than filing before your full retirement age for survivors. In this instance, you are entitled to your deceased spouse’s monthly benefit amount or 82.5% of the primary insurance amount.

I thought you said this was simpler?

I did. Imagine how much more complex filing early is!

For example, let’s say you begin benefits at your full retirement age for survivors, and your spouse claimed their benefits early at age 62. Let’s also say they were receiving a reduced amount of $1,600 per month instead of their primary insurance amount of $2,000 (which they would have received if they waited until full retirement age).

You will collect the larger of the two monthly numbers: your deceased spouse’s reduced monthly benefit of $1,600 or 82.5% of your deceased spouse’s primary insurance amount of $2,000. You would get $1,650 per month because 82.5% of $2,000 is larger than the reduced monthly benefit the spouse received while they were still alive.

Okay, now the fun part. If your deceased spouse started taking their benefits before their full retirement age, and you (the surviving spouse) start taking your spousal benefits before your full retirement age for survivors, the perfect storm happens, if you will.

If you have read some of my other articles, you have heard me mention William Reichenstein and William Meyer’s book, Social Security Strategies. Once again, they have produced the simplest and easiest way to explain how this works.

Three amounts will need to be calculated: first, the deceased’s retirement insurance benefit; second, 82.5% of the deceased’s primary insurance amount; and third, the reduced survivor’s insurance benefit. Then you need to take the lower number.

Take the same example above, except that the surviving spouse begins benefits at age 60 rather than waits until their full retirement age for survivors. Additionally, the deceased spouse claimed their benefits early at age 62.

They were receiving a reduced amount of $1,600 per month instead of their primary insurance amount of $2,000 they would have received if they waited until full retirement age. You will now have to use the following formula . . . .

Take the deceased’s reduced monthly benefit of $1,600 or 82.5% of their primary insurance amount, $2,000 (whichever is larger). This means the survivor would get $1,650 per month because 82.5% of $2,000 is larger than the reduced monthly benefit the spouse received while they were still alive.

Now you have to calculate the reduced survivor’s insurance benefit. To do that, you take the survivor’s benefit percentage at age 60 of 71.5% and multiply that by the deceased spouse’s primary insurance amount of $2,000, which equals $1,430.

Finally, you take the lower of the two. Therefore, the survivor’s monthly benefit would be $1,430.

See, that wasn’t so bad, LOL!

Many of the discussed scenarios assume the surviving spouse has a lower earnings record. To put it simply, the deceased spouse made more money than the surviving spouse during their lifetime.

What if I am divorced and my ex-spouse dies? Am I eligible for benefits?

The answer is yes, provided you were married for at least 10 years. You would be eligible for the same widow or widower benefits.

According to SSA.gov, if you remarry after age 60 (age 50 if you’re disabled), the remarriage will not affect your survivors’ benefits eligibility.

What should I do?

There are some interesting planning and claiming techniques that should be considered and analyzed. Naturally, it is not always a clear, easy decision. Hopefully, I can make things easier for you.

Generally, if the surviving spouse can grow their retirement benefits to exceed their survivors’ benefits, they would want to take survivors’ benefits first and then switch to their retirement benefits at age 70.

Suppose you cannot grow your retirement benefits at or by age 70 to exceed your survivors’ benefits. In that case, you want to do the exact opposite: begin your retirement benefits and switch to survivors benefits at the full retirement age for survivors.

The key here is waiting until full retirement age for survivors’ benefits, allowing you to take the maximum amount of benefits. This assumes you have not reached full retirement age for survivors.

Suppose you have attained full retirement age for survivors. In that case, you should simply determine if your retirement benefit is higher than your survivors’ benefit.

As we discussed, it is possible to let your retirement delay and accumulate credits to age 70, which may end up being more significant than your spousal benefit. If that is the case, you should switch to your retirement benefit at age 70. If not, you should just keep your survivors’ benefit for the rest of your life.

An easier decision is if the surviving spouse was the higher earner. Why is this easier? I am glad you asked. The survivors’ retirement benefits based on their earnings record can continue to receive delayed retirement credits until they begin up to age 70.

For example, suppose the surviving spouse has a full retirement age of 66, and they have not claimed their benefits yet. In that case, they can continue to delay until age 70 and keep receiving an approximate 8% growth on their benefits.

In the meantime, until they reach age 70, they can claim their survivors’ benefits while allowing their retirement benefits to accrue. Then, at age 70, they can switch from survivors benefits to retirement benefits.

I know what you’re thinking: What if I start taking my benefits and then my spouse dies? Can I stop my benefits so I can accrue delayed retirement credits to age 70?

Yes, if your spouse passes away in the first 12 months of you claiming your strategy. The Social Security Administration allows you to undo your decision and repay the benefits you received.

Case Studies

Case Study 1: The Higher Earner Dies First

- There is a husband and wife, and the husband dies and his monthly benefit is $2,200 per month.

- The surviving spouse is 66 years old.

- The surviving spouse has a primary insurance amount of $2,000. She has not started collecting benefits and will continue to accrue delayed credits of 8% per year until age 70.

- The full retirement age for retirement and survivors benefits are both at age 66 for her.

- This decision is simple: she should begin survivors benefits of $2,200 per month, and then at age 70 she should switch to her own benefits of $2,640.

| Age of Surviving Spouse | Survivor Benefit Monthly Payment | Her Own 2k Monthly Retirement Benefit |

|---|---|---|

| 66 | $2,200 | Accruing at 8% |

| 67 | $2,200 | Accruing at 8% |

| 68 | $2,200 | Accruing at 8% |

| 69 | $2,200 | Accruing at 8% |

| 70 | Payment stops | $2,640 |

| 71 | and switches to her | $2,640 |

| 72 | own benefit at age 70 | $2,640 |

| 73 | $2,640 | |

| 74 | $2,640 | |

| 75 | $2,640 | |

| 76 | $2,640 | |

| 77 | $2,640 | |

| 78 | $2,640 | |

| 79 | $2,640 | |

| 80 | $2,640 |

Case Study 2: The Lower Earner Dies First

- There is a husband and wife, and the husband dies and his monthly benefit is $1,500 per month.

- The surviving spouse is 66 years old.

- The surviving spouse has a primary insurance amount of $2,000. She has not started collecting benefits.

- The full retirement age for retirement and survivors benefits are both at age 66 for her.

- There are two different strategies that she should be exploring:

- Strategy 1: She begins her retirement benefits today of $2,000 per month for the rest of her life. She never exercises her survivors benefits.

- Strategy 2: She begins survivors benefits today at age 66 of $1,500 per month, and switches at age 70 to retirement benefits based on her earnings records of $2,640 per month. This strategy allows her benefits to accrue delayed credits of 8% per year until age 70.

- The break-even point where the second strategy starts to provide more cumulative benefits is at age 73. If she is in good health and has a longer life expectancy than age 73, the second strategy should be seriously considered.

| Age of Surviving Spouse | Survivor Benefit Monthly Payment Strategy 1 | Survivor Benefit Monthly Payment Strategy 2 | Annual Breakeven – Choosing Strategy 2 |

|---|---|---|---|

| 66 | $2,000 | $1,500 | ($6,000) |

| 67 | $2,000 | $1,500 | ($12,000) |

| 68 | $2,000 | $1,500 | ($18,000) |

| 69 | $2,000 | $1,500 | ($24,000) |

| 70 | $2,000 | $2,640 | ($16,320) |

| 71 | $2,000 | $2,640 | ($8,640) |

| 72 | $2,000 | $2,640 | ($960) |

| 73 | $2,000 | $2,640 | $6,720 |

| 74 | $2,000 | $2,640 | $14,400 |

| 75 | $2,000 | $2,640 | $22,080 |

| 76 | $2,000 | $2,640 | $29,760 |

| 77 | $2,000 | $2,640 | $37,440 |

| 78 | $2,000 | $2,640 | $45,120 |

| 79 | $2,000 | $2,640 | $52,800 |

| 80 | $2,000 | $2,640 | $60,480 |

Planning for spousal benefits is a difficult decision. While still living, what appears to be correct might not be the best decision for your spouse.