Why Knowing When to File for Social Security is Difficult — Really Difficult

I often get asked: “Joe, should I file early at age 62, or full retirement age (FRA), or delay to age 70?” My response is always the same. I know you can’t see me, but imagine me saying this with a big smile on my face: “Tell me when you are going to die.”

Most people are taken aback for a second and are like, “What did you say?” Then I explain that part of figuring out when to file is based on your life expectancy. If you are very healthy, your family history is such that both of your parents lived well into their 90s, and you can afford to delay until age 70 (the essential word being afford, more on this later in the article) than you should.

To put it simply, if you are going to pass away before age 70, start taking your benefits at age 62. If you live well past age 80, delaying benefits to age 70 is the way to go. The reality probably lies somewhere in-between for most things in life, when all the fun starts.

To simplify things, the concept we will assume in this analysis is that your full retirement age is 67.

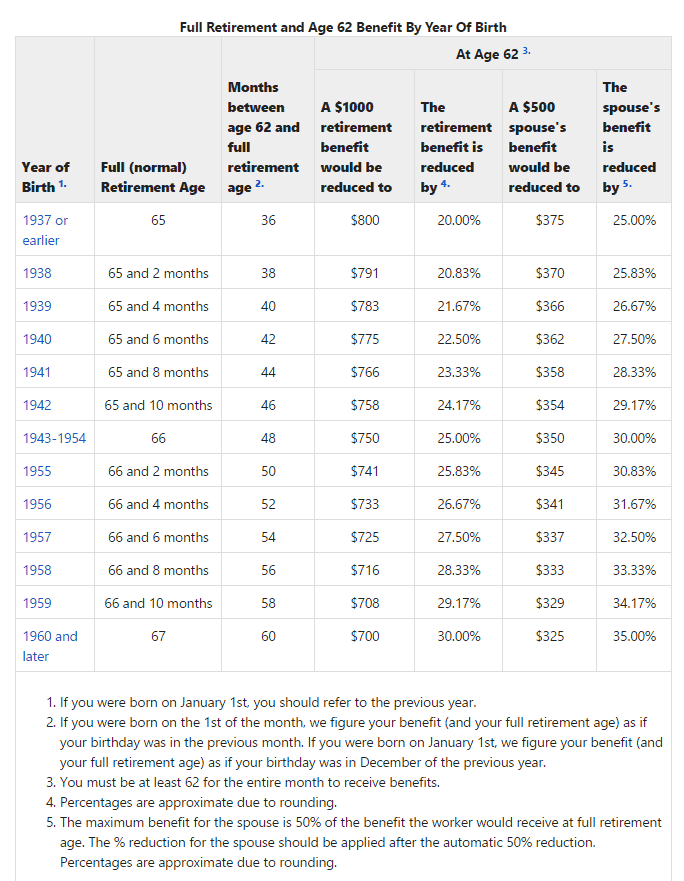

If you start at age 62, your benefits will be reduced by 30%! Yes, you read that correctly: 30%. Here is the breakdown according to SSA.gov:

Age 62 is approximately 30%.

Age 63 is approximately 25%.

Age 64 is approximately 20%.

Age 65 is approximately 13.3%.

Age 66 is approximately 6.7%.

For example, let’s take a hypothetical person born in 1960 or later — their FRA to receive full benefits is 67. If they were scheduled to receive $1,000 per month at age 67 and started collecting early at age 62, their benefit would be reduced to around $700 per month.

SSA.gov put out an excellent chart for the reduction in benefits for the different full retirement ages:

You will also need to be careful of the earnings test. The earnings test only applies to filers who have not reached full retirement age. In plain English, if you are still working and filing to receive benefits before your FRA, your Social Security benefits will most likely be reduced.

The Social Security Administration will deduct $1 from every $2 you earn above the annual. The limit for 2022 is $19,650. However, if you reach FRA in 2022, the limit on earnings for the months before FRA is $51,960.

So What Age Should I File as a Single Person?

Great question. I have no idea.

Huh?

I am sort of joking.

Should I file at age 62, 64, full retirement age, or delay filing to age 70?

William Reichenstein and William Meyer do a great job illustrating this in their book Social Security Strategies.

They illustrate that if a single individual (a single individual assumes that no one else can receive benefits based on the single’s earnings record) lives to age 80, the cumulative lifetime benefits will be approximately the same whether benefits begin at 62, 63, 64, or any age through 70.

Claiming the wrong strategy can be the difference of tens — if not hundreds — of thousands of dollars.

Every year you delay receiving benefits from your full retirement age to age 70, your benefits will increase by roughly 8% per year to age 70. FRA is the year you will receive full benefits. Please refer to my other article on full retirement age.

| Year of Birth* | Full Retirement Age (FRA) |

|---|---|

| 1937 or earlier | 65 |

| 1938 | 65 and 2 months |

| 1939 | 65 and 4 months |

| 1940 | 65 and 6 months |

| 1941 | 65 and 8 months |

| 1942 | 65 and 10 months |

| 1943-1954 | 66 |

| 1955 | 66 and 2 months |

| 1956 | 66 and 4 months |

| 1957 | 66 and 6 months |

| 1958 | 66 and 8 months |

| 1959 | 66 and 10 months |

| 1960 and Later | 67 |

| *If you were born on January 1st, you should refer to the previous year. (If you were born on the 1st of the month, Social Security figures your benefit (and your FRA) as if your birthday was in the previous month.) |

So why doesn’t everyone delay until age 70? I am glad you asked. It’s the same reason everyone does not file early at age 62. It all depends. To help explain things further, I am going to use a case study.

A Case Study

One of the most important factors (if not the most critical) when deciding when to take your benefit is the age you will die. Let’s look at a case study.

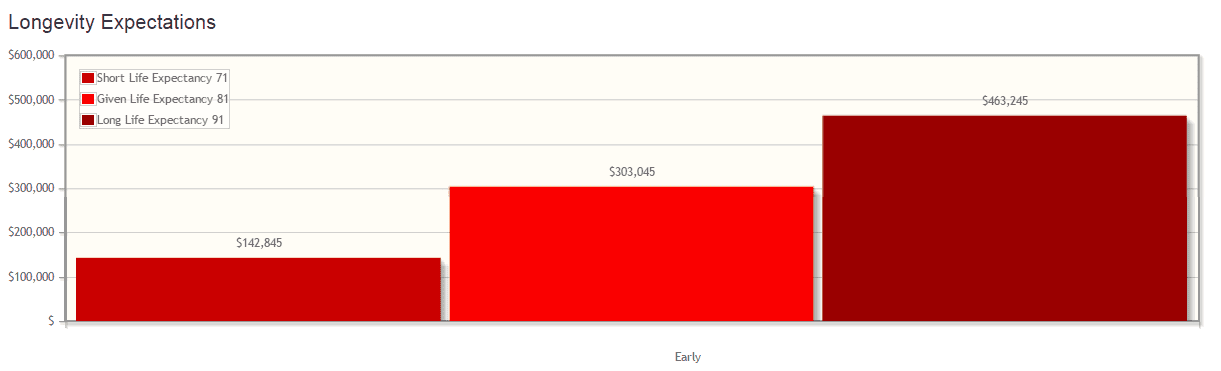

We have a single female, her date of birth is 10/14/1955, her full retirement age is 66 and two months, her estimated monthly benefit is $1,790, her life expectancy is 81, and for simplicity, we are not assuming inflation. I used a woman because women live longer than men (sorry, guys).

Claiming Benefits Early at Age 62

Her short life expectancy would be to age 71, and her cumulative benefits would be $142,845.

Her given life expectancy would be to age 81, and her cumulative benefits would be $303,045.

Her long life expectancy would be to age 91, and her cumulative benefits would be $463,245.

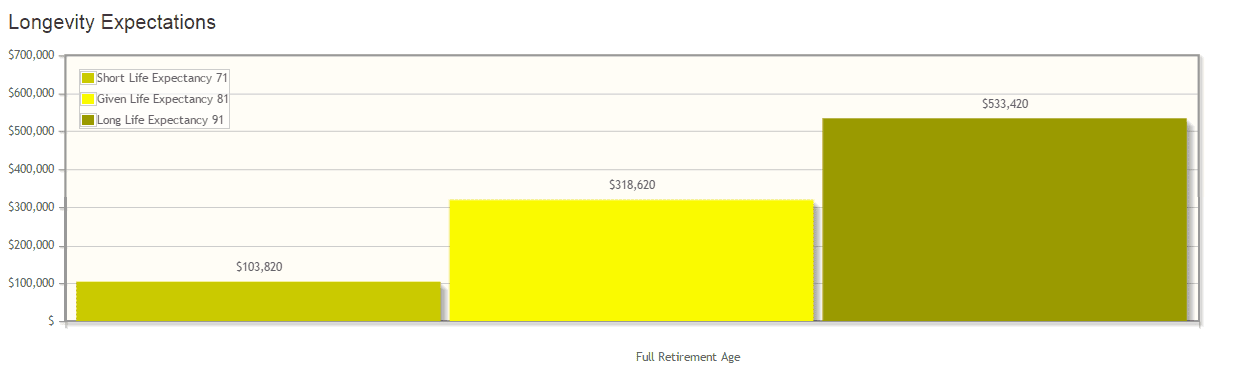

Claiming Benefits at Full Retirement Age (FRA): 66 and Two Months

Her short life expectancy would be to age 71, and her cumulative benefits would be $103,820.

Her given life expectancy would be to age 81, and her cumulative benefits would be $318,620.

Her long life expectancy would be to age 91, and her cumulative benefits would be $533,420.

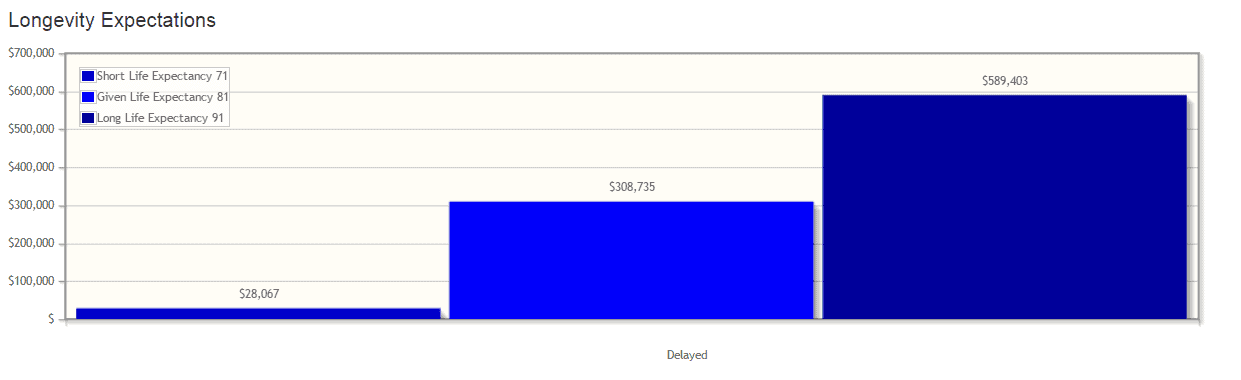

Delaying Claiming Benefits Until Age 70

Her short life expectancy would be to age 71, and her cumulative benefits would be $28,067.

Her given life expectancy would be to age 81, and her cumulative benefits would be $308,735.

Her long life expectancy would be to age 91, and her cumulative benefits would be $589,403.

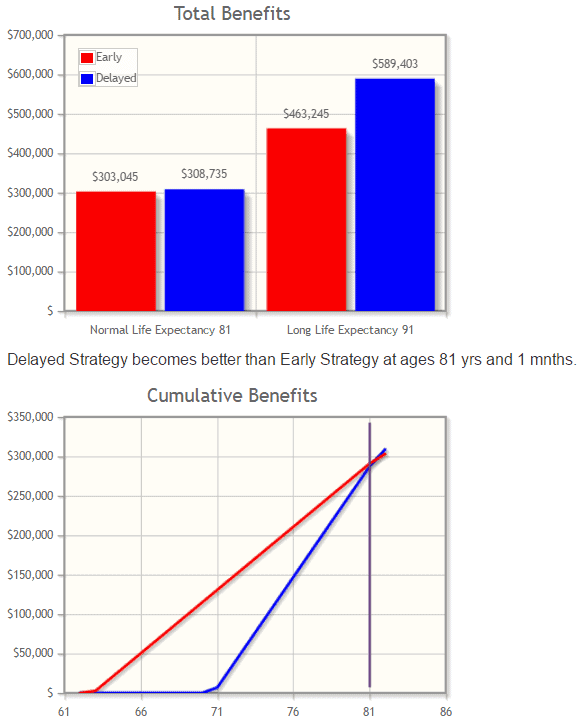

Case Study Analysis

As you can see, if she lives until her given life expectancy age of 81, then claiming early, at full retirement age 70, or delaying to age 70 does not make much of a difference. There is a difference of a few thousand dollars.

However, if she passes away suddenly at the age of 71, she clearly would have benefited from taking benefits early at age 62 (always remember to factor in the income earnings test, the case study was done assuming she was no longer working).

The same can be said if she lives to age 91 — the difference between claiming benefits at age 62 vs. age 70 is over $286,358 in cumulative benefits! I told you this decision was one of the most important you will ever make.

Another factor in determining when to claim benefits is the break-even crossover point.

Simply put, when delaying your filing will earn you more cumulative benefits. If you look at the illustration above, the crossover point is 81 years and one month.

Remember, even though your monthly benefit is higher, if you delay benefits to age 70, by filing early at age 62, you receive eight years of payments before your payments begin at age 70. Those payments need to be accounted for when analyzing what age to file.

Strategies for Couples

Joe, I have a spouse. What should I do? Is it different from the single filer’s strategies?

Determining the best and most efficient strategies should focus on spousal and survivor benefits. Married couples not only have to figure out the best-claiming plan based on the rules and case study we just discussed, but you also need to factor in how it will affect your spouse.

If you are single, I have great news! You can skip this section because it does not pertain to you.

Before we get into specific case studies and strategies, we first must understand what spousal benefits are.

Spousal Benefits

Spousal benefits are the benefits your husband or wife receives based on your earnings record when you are alive. Survivor benefits are benefits the husband or wife receives after they have died.

You guessed it; survivor benefits have a whole different set of rules. I got your back and have written an article specifically about survivor benefits.

What is your earnings record? According to SSA.gov, it is a chronological history of the amount of money you earned each year during your working lifetime.

I will be specifically referring to the spouse with the lower earnings record, which is just a fancier way of saying the spouse that earned less money than the other spouse. It could be the husband or wife; it does not matter.

Here are the rules for qualifying for spousal benefits. You must be either:

- at least 62 years of age.

- any age and caring for a child entitled to receive benefits on your spouse’s record who is younger than age 16 or disabled.

Understand File and Suspend

This claiming option involved one spouse (usually the higher earner once they reach full retirement age) filing for benefits and immediately suspending the payments.

The purpose was to allow the worker’s spouse to begin a spousal benefit while the worker’s benefit continued to earn delayed retirement credit on their record. This great strategy is no longer available as of April 30, 2016, thanks to the Bipartisan Budget Act of 2015.

Currently, a spouse can only claim spousal benefits when the higher-earning spouse has already claimed them first.

Dual Entitlement

The spouse is entitled to the larger of the benefits based on their earnings record or, if eligible, spousal benefits, which is up to 50% of the spouse’s primary insurance amount.

Suppose you are eligible for your retirement and spousal benefits. In that case, the Social Security Administration will pay your benefits based on your earnings records first.

Suppose your spousal benefit is higher than your benefits. In that case, you will get a combination of benefits equaling the higher spouse benefit.

Many people often ask me: “What about my spouse?” Is she entitled to half of my benefits even though they did not work? The answer is yes! They would be allowed to half of the spouse’s benefit. Naturally, many rules and factors come into play.

Let’s look at an example. John and Mary have been married for over 35 years. John’s primary insurance amount at his full retirement age is $2,000 per month, and Mary never worked. Even though Mary does not have any earnings record, she is entitled to receive $1,000 per month at her full retirement age.

Does the spouse need to wait until full retirement age to receive the benefit? No. In this example, Mary could take her benefit at age 62, just like in the single filer examples; her benefit would be reduced. How much will her benefit be reduced? I suggest reading my article, The Basics: Full Retirement Age and Social Security.

Let’s use the same example but change things up a bit. Let’s assume that Mary worked her whole life and her primary insurance amount at her full retirement age is $700 per month. When Mary goes to file at her full retirement age, the Social Security Administration will pay her $700 per month benefit. They will add the additional $300 per month to get her up to 50% of John’s benefit.

Please keep in mind that for Mary to receive spousal benefits, her husband John must have filed and received benefits or must have filed and immediately suspended them. In other words, Mary would not be able to start collecting her benefits early at age 62 or even at full retirement age if John has not filed for his yet.

What if I’m Divorced

You can still qualify for spousal benefits. If you were married to your ex-spouse for at least 10 years, you might be eligible to receive spousal benefits. You guessed it; there are many rules and scenarios. I will have an article specifically for divorced strategies.